Editorial Note: Forbes may earn a commission on sales made from partner links on this page.- test default

Mobile only banks are gaining traction against their traditional brethren, aiming to disrupt the financial services market with zero fees, higher deposit interest rates, and mobile and Internet account openings. One of the digital-only banks that has been making a splash is Ally Bank, the Detroit, Michigan-based unit of Ally Financial. Its parent company has been around since the 1920’s, but it was immediately after the financial crisis of 2008-2009 that it decided it was time to create a different type of bank.

Out of that came Ally Bank, which it says was developed with three principles in mind: do right, talk straight and be better. Since then the bank has grown and as of the second-quarter of 2018 had deposits of $98.7 billion with more than 1.5 million customers banking with it.

Like the other digital online banks, Ally Bank is good for consumers who are comfortable banking from their smartphone or desktop computer, are focused on avoiding bank account fees and is looking to get the most out of their deposits. If you favor face-to-face interactions with your bank and need or want more high-end banking features this Internet bank may not be right for you.

Interest Earning Checking

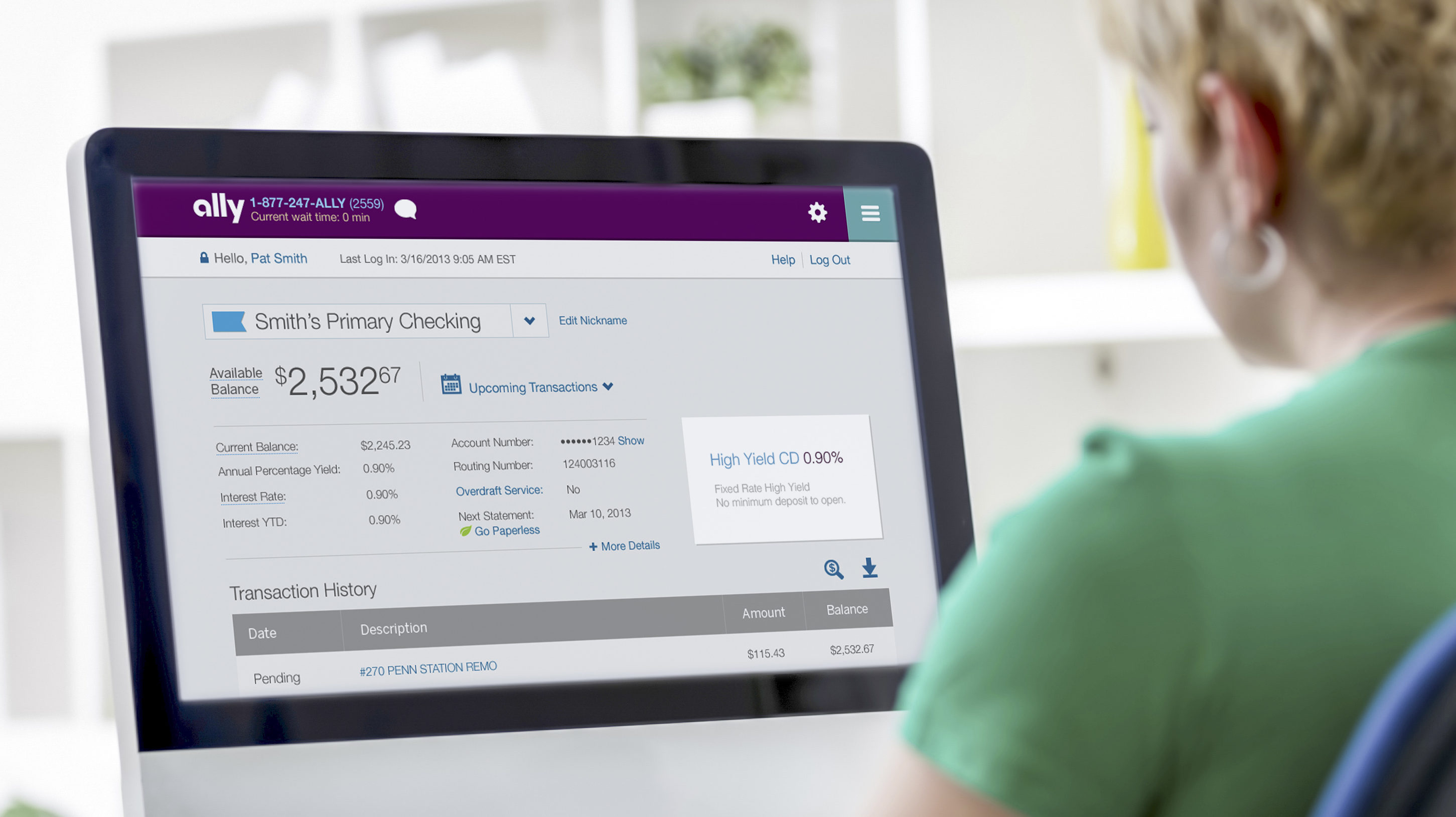

One of the advantages of not having any physical branches is that the bank can pass along those savings to customers in the form of little to no fees. That is the case with the Ally Interest Checking Account, the only checking product offered by this online bank. There are no monthly fees associated with the account nor is there a minimum deposit to open an account.

Customers also get free standard checks, a free debit card and access to a free bill pay service. Customers who use an Allpoint ATM never face any charges. Go outside of that ATM network of 55,000 ATMs and Ally will reimburse you up to $10 per statement cycle. Because there are no physical branches, customers have to rely on technology when depositing checks and that is where the Ally eCheck Deposit feature comes in.

Using the camera on your mobile phone you take a picture of the check and then deposit it. Old-school customers can mail in deposits with postage paid envelopes. Ally also supports Zelle, the peer-to-peer payment platform that enables you to send or receive money from friends and family.

Ally Bank pays a 0.10% annual percentage yield or APY on accounts with a less than a $15,000 daily balance and 0.60% APY accounts for those accounts with more than $15,000. The latter is higher than some of its traditional rivals. Capital One 360 Checking Account pays an APY of 0.20% while Wells Fargo has a 0.01% APY on its checking account for balances under $5,000 and 0.05% for accounts with balances higher than that.

Ally Bank does charge a $25 fee for an overdraft item paid or returned but caps it at one per day. That means you won’t get hit each time you bounce a check on the same day. You can also set up direct deposit with this account.

Savings & Money Market Accounts

One of the allures of online banks is that when it comes to the APY on savings deposits and certificates of deposit, they tend to pay a higher rate. You won’t get rich off the APY thanks to the low-interest rate environment, but you can do better on your savings lots of the time than with a traditional bank. As it stands Ally Bank pays an APY of 2.20% on all balances on its online saving account.

There are no monthly fees associated with the savings account. Customers can only make deposits via their smartphone or by mailing it in but with the interest compounding daily you do get to earn a little more on your savings. The more often your money compounds, the more money you make. Interest can compound daily, monthly and annually. The deposits are FDIC insured which means your money is protected up to $250,000 if the bank were to go under. While there are no monthly maintenance fees, you are limited to six transactions per statement cycle. After that it’s $10 per every outbound transfer.

In addition to a savings account, Ally Bank also offers a money market account which pays an APY of 0.90% on a daily basis. Have $25,000 or more in the account and that gets bumped up to 1.00% APY. Customers pay no monthly fees with this account, are able to make unlimited deposits and ATM withdrawals for free. They are also allowed six additional transactions each month. Just like the savings account, deposits are FDIC insured and interest is compounded daily.

High Yield Certificate of Deposit or CD

When it comes to CDs, Ally Bank is fully represented offering varying terms and APYs to meet every savers’ needs. Rule of thumb: the longer your money is in the CD the higher APY you get. At Ally Bank, a 5-year CD pays an APY of 3.10% while a 3-year CD has an APY of between 2.60% to 2.75% depending on the opening deposit. These are riskier in a rising interest rate environment and thus the higher APY. After all if you lock up your money for say 60 months, you could miss out on a higher paying opportunity as interest rates rise.

On the short end of the range, Ally’s 3-month CD pays an APY of just 0.75% the 6-month CD pays 1.00% APY while a 9-month CD will get you 1.25% APY. Looking to lock up your money for 12 months and the CD will pay you APY of 2.75%. A 18-month CD has an APY of between 2.50% and 2.75% depending on the opening balance.

Ally Bank also offers a raise your rate CD which gives savers the opportunity to increase their rate once over the 2-year term or twice if they purchase a 4-year term CD. The APY on these products is 2.60%. For savers looking for even more protection in a rising rate environment Ally has the no penalty CD which pays an APY of between 1.80% and 2.30% depending on the opening deposit. With this product, customers can withdraw money without having to face any penalties. You can start drawing down your money on the seventh day following the funding of the CD.

Ease Of Use

Lots of people still value a human relationship when it comes to banking but scores of others balk at even walking into a branch. Ally Bank makes it easy for the latter, relying on technology to amp up the convenience factor. In addition to enabling customers to remotely make deposits via their mobile phone’s camera, Ally Financial has created a skill for Alexa, Amazon.com’s voice-activated digital assistant.

That means customers with an Alexa enabled device can use voice commands to check balances on their checking, savings, money market, and CD accounts, transfer money, hear recent transactions and get the current rates on its products. Still, crave some human intervention? Ally Bank has 24/7 customers service support via phone or live chat that is staffed with real human beings.

For people who don’t need the human touch and are looking for a decent return on their savings, Ally Bank makes a lot of sense. If you have a lot of complex needs, want to deal with people face to face and aren’t comfortable with technology then this online-only bank isn’t for you.